Featured

Table of Contents

Financial obligation debt consolidation with an individual loan offers a couple of benefits: Fixed interest rate and payment. Personal loan debt combination loan rates are usually lower than credit card rates.

Customers typically get too comfy simply making the minimum payments on their charge card, but this does little to pay down the balance. Making just the minimum payment can cause your credit card financial obligation to hang around for decades, even if you stop utilizing the card. If you owe $10,000 on a charge card, pay the typical credit card rate of 17%, and make a minimum payment of $200, it would take 88 months to pay it off.

Contrast that with a debt consolidation loan. With a financial obligation combination loan rate of 10% and a five-year term, your payment only increases by $12, however you'll be devoid of your debt in 60 months and pay just $2,748 in interest. You can use a personal loan calculator to see what payments and interest may appear like for your financial obligation combination loan.

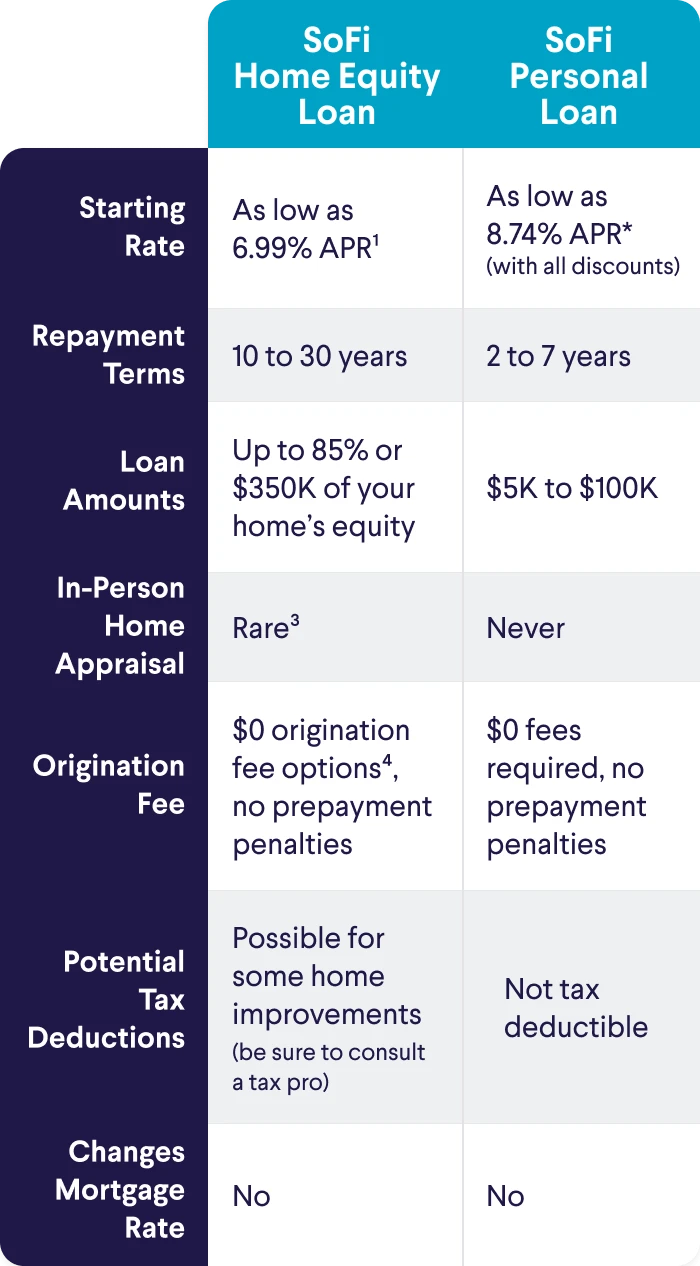

The rate you get on your individual loan depends upon many elements, including your credit rating and income. The most intelligent way to know if you're getting the best loan rate is to compare deals from competing lenders. The rate you receive on your financial obligation combination loan depends upon numerous factors, including your credit history and earnings.

Debt debt consolidation with an individual loan might be ideal for you if you meet these requirements: You are disciplined enough to stop carrying balances on your credit cards. If all of those things don't apply to you, you might need to look for alternative ways to combine your debt.

How to Consolidate Credit Card Debt in 2026

In some cases, it can make a financial obligation issue worse. Before consolidating financial obligation with a personal loan, consider if one of the following circumstances applies to you. You understand yourself. If you are not 100% sure of your ability to leave your credit cards alone once you pay them off, don't combine financial obligation with a personal loan.

Individual loan interest rates typical about 7% lower than credit cards for the exact same borrower. If you have credit cards with low or even 0% initial interest rates, it would be silly to change them with a more pricey loan.

In that case, you may wish to use a credit card debt combination loan to pay it off before the charge rate begins. If you are just squeaking by making the minimum payment on a fistful of credit cards, you may not be able to reduce your payment with a personal loan.

This optimizes their profits as long as you make the minimum payment. An individual loan is developed to be settled after a specific variety of months. That might increase your payment even if your rate of interest drops. For those who can't take advantage of a debt consolidation loan, there are options.

Best Ways to Pay Off Debt in 2026

If you can clear your financial obligation in fewer than 18 months approximately, a balance transfer credit card could provide a faster and cheaper alternative to a personal loan. Consumers with excellent credit can get up to 18 months interest-free. The transfer charge is typically about 3%. Make certain that you clear your balance in time, nevertheless.

If a financial obligation consolidation payment is too high, one method to lower it is to stretch out the repayment term. That's since the loan is protected by your home.

Here's a contrast: A $5,000 personal loan for financial obligation consolidation with a five-year term and a 10% interest rate has a $106 payment. A 15-year, 7% interest rate 2nd mortgage for $5,000 has a $45 payment. Here's the catch: The overall interest expense of the five-year loan is $1,374. The 15-year loan interest expense is $3,089.

How to Consolidate High Interest Debt in 2026

If you truly need to lower your payments, a 2nd mortgage is a good choice. A debt management strategy, or DMP, is a program under which you make a single monthly payment to a credit counselor or debt management specialist.

When you get in into a plan, understand just how much of what you pay monthly will go to your financial institutions and just how much will go to the business. Learn the length of time it will take to end up being debt-free and make sure you can pay for the payment. Chapter 13 bankruptcy is a debt management plan.

One benefit is that with Chapter 13, your financial institutions need to participate. They can't choose out the method they can with debt management or settlement strategies. Once you file bankruptcy, the personal bankruptcy trustee determines what you can reasonably afford and sets your monthly payment. The trustee distributes your payment among your creditors.

Released amounts are not gross income. Financial obligation settlement, if effective, can unload your account balances, collections, and other unsecured debt for less than you owe. You usually offer a lump sum and ask the financial institution to accept it as payment-in-full and cross out the staying overdue balance. If you are extremely a great arbitrator, you can pay about 50 cents on the dollar and bring out the financial obligation reported "paid as concurred" on your credit rating.

2026 Analyses of Credit Counseling Programs

That is extremely bad for your credit history and score. Chapter 7 bankruptcy is the legal, public variation of financial obligation settlement.

Financial obligation settlement permits you to keep all of your ownerships. With personal bankruptcy, discharged financial obligation is not taxable earnings.

Follow these tips to ensure a successful debt repayment: Find an individual loan with a lower interest rate than you're currently paying. In some cases, to repay debt rapidly, your payment needs to increase.

{kind=link}

Latest Posts

How Professional Programs Manage Payments in 2026

Benefits of Nonprofit Debt Programs in 2026

How to Combine Credit Card Debt in 2026